This article is an extract from the GIC Report FY2019/2020. You may read the full Report here.

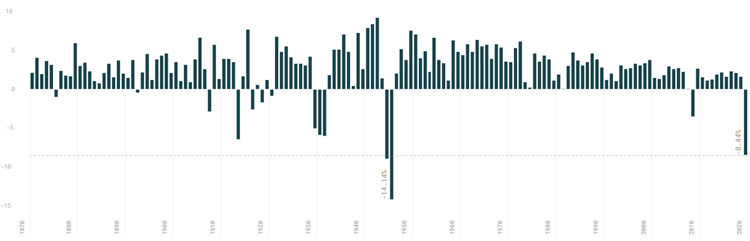

The global community is facing a public health crisis, an economic crisis, and financial turmoil all at once — an unprecedented combination in modern times. Extreme safe-distancing measures have resulted in the deepest global downturn since World War II (Figure 1). The outlook for the investment environment is particularly uncertain. The crisis has also brought to the fore the market vulnerabilities that GIC had highlighted in previous annual reports, and accelerated several shifts that could shape the global investment landscape going forward.

Source: International Monetary Fund (IMF), Jorda, Schularick & Taylor, Macrohistory Database, GIC Calculations

Prior to COVID-19, our view was that asset prices were not providing adequate compensation for the level of risk that we were facing, given weakening fundamentals, limited policy room and growing geopolitical uncertainties. This led us to reduce the overall risk in the portfolio, and stress-test our portfolio and investments against potential adverse scenarios.

This defensive stance helped cushion the portfolio during the worst of the financial market volatility in the first quarter of 2020. While the low-growth, low-productivity and fraught geopolitical environment is expected to persist, there are several major shifts that will likely result in lower future returns and increased volatility in the markets.

I. Uncharted policymaking given high debt levels and low interest rates

High debt and low interest rates

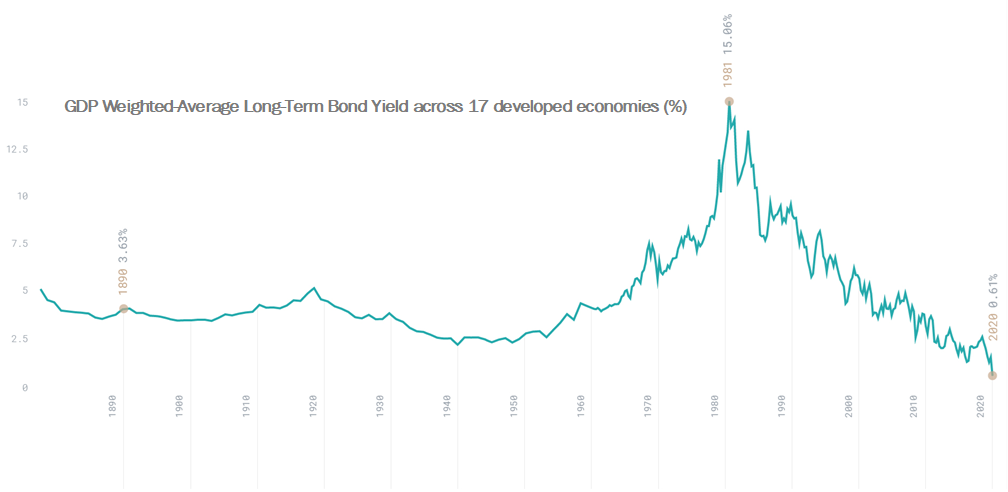

Pre-crisis, long-term interest rates globally were already at their lowest levels for at least 140 years (Figure 2). This was not just a result of central bank policy, but also longer-term trends, such as slower population growth, weaker productivity growth, and an excess of savings over investment.

Source: Jorda, Schularick & Taylor, Macrobond Financial AB, GIC Calculations

The low interest rates contributed to steadily increasing levels of debt as companies were increasingly incentivised to restructure balance sheets away from equity and towards debt. “Share buybacks” were a key support for equity markets, particularly in the US. However, the financing of the share buybacks through the issuance of debt increased balance sheet fragility.

As the world emerges from this crisis, the aggregate debt burden will be higher still. Companies will have to borrow even more to weather the collapse in revenue during the economic slowdown. The large and rapid response by policymakers globally has also sharply increased public debt levels and shifted risk onto government balance sheets. Such elevated levels of debt in turn limits the extent interest rates could rise without causing a significant slowdown in the economy.

To date, the rapid policy response and fall in interest rates have helped boost asset prices and reduce the likelihood of a deep financial crisis. With policy interest rates at or already below zero, central banks have had to resort to increasingly unconventional measures to support the economy. In many countries, central banks have increased the range of assets purchased and reduced the quality of collateral needed.

Paradigm shifts in policymaking

Two fundamental changes are happening to policymaking.

The first relates to monetary policy. The major central banks are now unlikely to respond pre-emptively to signs of higher inflation and are instead willing to accommodate periods of above-target inflation. This is a marked change from the past when interest rates were usually raised in response to leading indicators of inflation, which subsequently dampened economic activity.

The second is the bigger role played by fiscal policy in stimulating the economy, given limited policy room for central banks to cut rates. The size of fiscal stimulus packages is expected to be US$11 trillion, almost 20% of GDP for advanced economies and about 5% of GDP for emerging economies. Alongside the impact of lower tax revenues and higher government transfers due to the deep recession, these stimulus packages are expected to contribute to an increase in public debt of around 19% of global GDP in 2020 alone.

Not all countries can afford such large-scale stimulus, and concerns over how these programmes are financed will likely weigh on debt markets, particularly in lower-income economies and those that are reliant on foreign capital flows. Relatedly, there is also greater implicit or explicit cooperation with monetary policy in either leveraging up fiscal programmes, increasing purchases of government debt, or keeping financing costs for the government low. While these coordinated monetary and fiscal policies have been critical in supporting the economy, they may prove difficult to calibrate and reverse in some cases once the economy normalises.

These shifts in policymaking have the potential to change the investment environment in two ways.

- Increased risk of higher inflation over the medium term: If central banks deliberately keep rates low even as economic activity increases, economies could overheat, resulting in upward pressure on prices. This risk scenario is only likely to play out over the medium term given the strong disinflationary forces in the present environment. Should it materialise, however, it would imply a very different investment landscape relative to what investors have been used to. In particular, the correlation between equities and bonds could become positive, making it difficult for asset allocators to achieve diversification.

- Currency moves could play a larger role in asset returns for a global investor: As the effectiveness of the interest rate channel for monetary policy decreases, more emphasis will be placed on increasing purchases of government debt and potentially capping interest rates, which could lead to capital flight and currency depreciation.

These shifts are taking place at different degrees in different countries and regions. Understanding and getting ahead of these developments will be key for investors to navigate the investment environment.

II. Intensified headwinds for globalisation

A major theme emerging out of the COVID-19 crisis is the increasing emphasis by corporates on resilience. Companies are re-thinking their global supply chains to increase reliability and reduce complexity. They will likely accelerate the adoption of technology such as advanced robotics and additive manufacturing as well as digitalisation of content. This will help shorten supply chains and reduce the exposure of goods production to trade. Companies will also look to diversify their production geographically, or bring production closer to home. In the post-COVID-19 world, global supply chains are likely to undergo significant structural change. Changes in national policies also play a role. National security concerns have already led to pressure to re-shore supply chains for products such as pharmaceuticals, medical equipment, and technology. Restrictions on the movement of labour and capital could also tighten to protect domestic interests.

Strains in the US-China relationship will remain a significant headwind, with tensions rising in the run-up to the November 2020 US presidential elections. There could be further restrictions related to technology, with the US already excluding Chinese firms from its Information and Communications Technology supply chains, and limiting China’s access to US-origin technology and materials. Strategic sectors such as healthcare and defence are likely to see more re-shoring to the US. In response, China’s strategy is to globalise in specific sectors such as healthcare, substitute local suppliers for US IT sector suppliers, and get closer to large end-markets like the US by producing in Mexico.

In some ways, these shifts will lead to a more robust system. Manufacturers that used to run very lean processes are considering introducing redundancies into their systems. Companies are also diversifying their suppliers, and standardising parts and processes to make them more modular and easily replaceable with alternatives. While these are not new considerations for global manufacturers, the crisis has highlighted the necessity and urgency of moving forward on these changes. These shifts will help ensure a more secure and stable supply of goods and products.

However, a major retreat in globalisation would hurt productivity growth by preventing:

- more efficient global allocation of resources,

- more competition between companies, and

- knowledge and technology transfers.

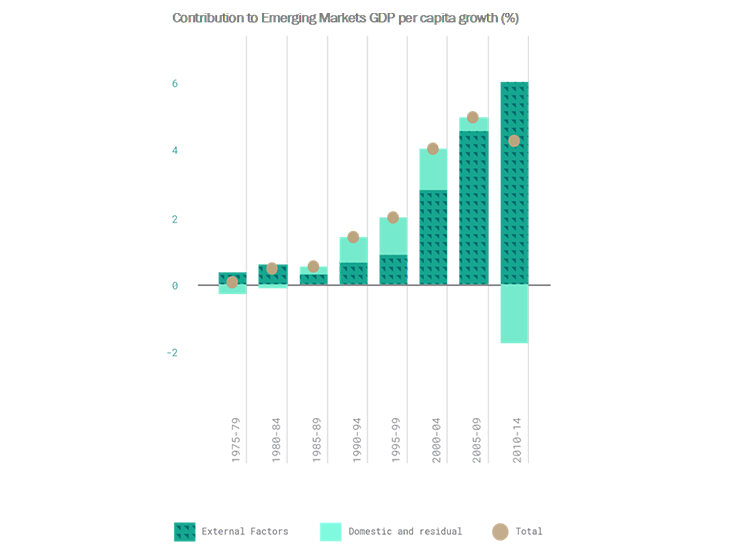

It would also reduce businesses’ access to cheaper and higher quality inputs, and consumers’ access to lower prices and a greater variety of products and services. This could be especially detrimental to emerging markets that have historically relied on a more export- and foreign investment-led growth model (Figure 3).

Source: The International Monetary Fund

III. Asia to see rising headwinds, but still outperform over the long term

As highlighted in the GIC Report 2018/19 Feature Article, “Asia’s Growing Importance in the Global Economy and Financial Markets”, GIC has been committed to Asia’s growth story for over three decades. Our belief in Asia’s resilience rests not only in the region’s improving institutions and macroeconomic policies, but also growth in exports and intra-regional trade. However, there are important differences across Asian economies with respect to the level of development, economic structures, and institutional capabilities. The capabilities to deal with the pandemic also differ across the region, which could imply a less synchronous recovery. Country differentiation is, consequently, even more important.

The hit from the COVID-19 outbreak to Asia’s economic growth has been significant. For instance, China’s GDP contracted by 6.8% year-on-year in the first quarter of 2020. A number of Asian countries were quick to introduce strict virus containment measures and sizeable policy support, which have to date shown efficacy in flattening the virus curve for a number of countries, including China and South Korea.

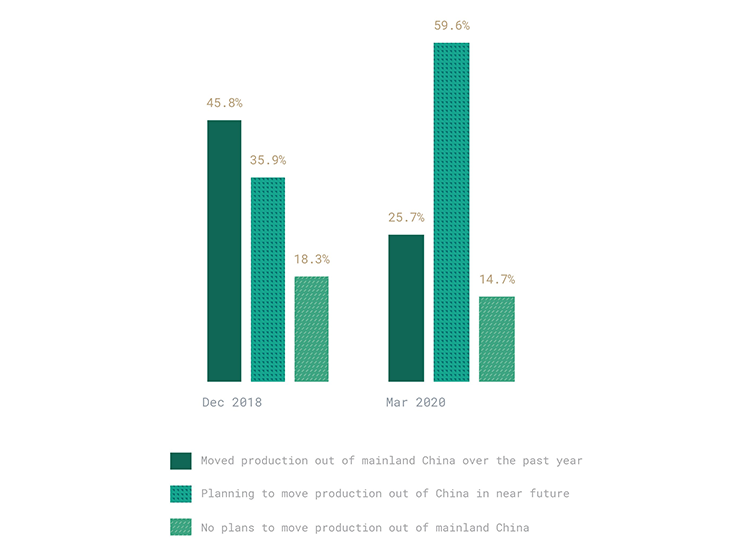

The economic recovery will take time as supply normalisation will be gradual, precautionary savings will stay high, and external demand will remain subdued given the different stages of virus transmission across markets and possible subsequent waves of infection. As discussed in the previous section, some diversification of global supply chains to avoid heavy concentration on production from China is also likely to accelerate (Figure 4).

While some of this will result in re-shoring production to home markets, many companies are turning to other Asian economies, like Taiwan, India, and ASEAN, as alternatives. For example, registered foreign direct investment in Vietnam has picked up pace since the US-China trade war started in late-2018.

Source: UBS Evidence Lab – Impact of Trade War on Japan, South Korea and Taiwan Manufacturers B2B Survey

As we have seen in the past, even in the face of large uncertainties, the Asian governments, businesses, and people have shown the resourcefulness to adapt and adjust their growth models. The handling of the COVID-19 crisis also demonstrated the maturity in Asia’s institutions and governance. We believe that investment in healthcare systems will increase in coming years, with positive knock-on effects in terms of preparedness for future pandemics, higher life expectancy and improved quality of life.

Over the longer term, Asia can continue to derive solid growth from:

- urbanisation and middle-income growth,

- investments in infrastructure and human capital, and

- deeper regional integration of economies and capital markets.

While headline risks have indeed risen, these factors should continue to generate self-sustaining growth in Asia, including China, and drive its out-performance over the long term. However, given the challenges going forward, including from increasing headwinds to globalisation, it is imperative that governments across the region are steadfast in their efforts to introduce structural reforms that can help support the potential growth rates of their economies and their adaptability to an ever-changing global economic landscape.

IV. Industry consolidation to increase

The COVID-19 crisis has drastically weakened the finances of many companies, particularly small- to medium-sized ones. Many will be forced to file for bankruptcy, secure additional funding, or seek mergers or other strategic alternatives. While fiscal packages have been introduced to provide support to the corporate sector, the default rate of global listed companies has already risen to the highest level since the Global Financial Crisis. This will continue to rise in the near term and could accelerate should the crisis prolong.

The markets reflect these dynamics with investors showing a strong preference for companies with more resilient balance sheets and business models. Smaller companies may be particularly vulnerable to consolidation. Many came into this crisis with high leverage, while also facing rising competitive pressures including technological disruption. Barring regulatory action, large companies, with stronger financials and technological advantages, may be better positioned to become even bigger and stronger.

In addition, private equity dry powder reached record highs (Figure 5) in June 2020, providing further support for industry consolidation going forward. Long-term investors could also play an important role in providing capital to sustain good businesses through these difficult times.

Source: Preqin

How is GIC responding to this changing environment?

Periodic crises are a feature of global financial markets and an unavoidable facet of investing for the long term. The lessons learnt from GIC’s past investment history help us improve our responses to current challenges.

First and foremost, we must have a deep understanding of who we are, including our mandate, values, risk capacity, capabilities, and constraints. This in turn drives our two key investment principles. Prepare, not Predict, and Focus on the Long Term.

- Prepare, not Predict: To prepare for a wide range of potential outcomes with high downside risks, we stress-test our assumptions as well as consensus beliefs against a range of alternative scenarios. Diversification is key to constructing a resilient portfolio. We need to remain humble, recognising that there is much we do not know about the changing and unpredictable future. At the same time, we continue striving to learn as much as we can to respond as best we can.

- Focus on the Long Term: This is integral to our mandate and investment approach. We emphasise fundamental trends over market sentiments, given the expectation that with the fullness of time, investment returns would reflect the fundamentals. We also continue to build on our long-term partnerships and capabilities to provide flexible capital.

With the conditions of high asset valuation and profound uncertainty across a wide range of structural issues as described above, we face an elevated risk of permanent portfolio impairment. Hence, our first order of business is to contain that risk at the overall portfolio level. In addition, when underwriting investment deals, we need to emphasise resilience and optionality, and yet be prepared to take advantage of market volatility if there are attractive risk-reward opportunities.

Finally, we need to maintain organizational resilience. Our considerable business continuity planning was tested by the unique nature of this pandemic, which not only triggered extreme market volatility but also affected our operations across our 10 offices. As the impact of COVID-19 is likely to last for some time, and such ‘known unknown’ events could also become more common in the future, we need to ensure that our operations, digital infrastructure and people are able to sustain performance, especially through such challenging times.

The investment uncertainties that result from the COVID-19 pandemic will require vigilance, agility, and resilience for the journey ahead. We continue to adhere to our core values and investment principles, refine our playbook and processes, and do our best to achieve steady long-term returns on the reserves under our management.