This article was written by Freddy Orchard, who is a consultant and author of ‘Safeguarding the Future’. He has been director of Economics at the Monetary Authority of Singapore (1995-1997) and GIC (1989-1999). He currently sits on the investment committees of several Singapore charities.

The term “Sovereign Wealth Fund” (SWF) was coined by financial analyst Andrew Rozanov in his 2005 article “Who Holds the Wealth of Nations?”, to demarcate an emerging breed of state-owned investment funds from other institutional investors. Since then, the term has gained wide usage and SWFs have been acknowledged as a significant investor group.

What is a sovereign wealth fund?

While every SWF has its own unique features, the essence of a SWF is that it is state-owned and mandated to invest the public funds under its charge.

The focus on investing is what differentiates a SWF from a central bank. Central banks hold foreign exchange reserves, essentially to implement exchange rate policy. They also have other functions such as supervising the financial system. A SWF by contrast is primarily an investment management entity enjoined to grow its assets under management (AUM). SWFs invest in a wide range of asset classes such as bonds, listed equity, real estate, private equity and infrastructure. Their asset allocation policy and risk posture will vary with the purpose of the funds they manage.

Depending on their funding source, SWFs can be classified as either commodity or non-commodity based. Commodity-based SWFs include those from oil-producing countries such as the Arab Gulf states, Russia, Brunei and Norway. Non-oil commodity producers include Chile which is funded mainly from copper mining royalties, and Botswana from diamonds and mineral royalties.

In contrast, non-commodity SWFs are funded from reserves accumulated through non- commodity exports, capital inflows, budget surpluses, land sales and public savings, and the privatisation of state-owned enterprises. Most Asian SWFs are in this category, like Singapore, China and South Korea. The share of AUM by non- commodity based SWFs rose from 39% to 48% over the 10 years to 2018.

SWFs vary considerably in size, from Norway’s Government Pension Fund Global (GPFG), which is reported to have the largest AUM at around US$1.1 trillion (end 2019), to SWFs with AUM of less than US$1 billion. SWF wealth is also heavily concentrated, with the top 10 holding about 80% of the combined SWF AUM. Asian and Middle Eastern SWFs each account for 40% of the total AUM of SWFs and European SWFs another 13%.

Several SWFs, like Singapore’s GIC, Norway’s GPFG and Kuwait’s Kuwait Investment Authority (KIA), only invest internationally. Meanwhile, there are SWFs like Malaysia’s Khazanah Nasional and Abu Dhabi’s Mubadala which invest both domestically and internationally.

Different types of sovereign wealth funds

The International Monetary Fund (IMF) categorises SWFs into five types, each with a specific purpose, though many have objectives that straddle several categories:

- Reserve Investment funds focus on generating returns from their investments. The China Investment Corporation (CIC) and Korea Investment Fund (KIC) are examples.

- Stabilisation funds typically found in commodity-exporting countries are used to cushion the economy from potentially destabilising effects of large fluctuations in commodity prices. For example, Ghana’s Stabilization Fund and Chile’s Economic and Social Stabilization Fund.

- Future Generation funds embody the pursuit of intergenerational equity. Many oil-producing countries have such funds to invest their oil revenues to assure a stream of income for future generations when their oil fields are depleted. Examples are Abu Dhabi Investment Authority (ADIA), Alaska’s Permanent Fund and KIA’s Future Generations Fund. Some non-commodity countries also adopt the intergenerational equity principle for their SWFs. This includes Singapore - where half of the expected long-term real returns from the reserves have to be retained for future generations>>.

- Development funds invest with the twin objectives of producing financial returns and developing the local economy and attracting foreign investment. An example is Abu Dhabi’s Mubadala Investment Company, which promotes the diversification of the Abu Dhabi economy so that it will be less reliant on oil over time. Mubadala has co-invested with Softbank in a fund to attract reputable start-ups to a technology hub in Abu Dhabi.

- Contingent Pension Reserve funds are designed to enable Governments to meet the liabilities of their social welfare and public pensions systems Examples are Norway’s GPFG, Australia’s Future Fund and New Zealand’s Superannuation Fund.

A country can also have more than one SWF with different objectives. For instance, Abu Dhabi has its ADIA and Mubadala.

The emergence of sovereign wealth funds

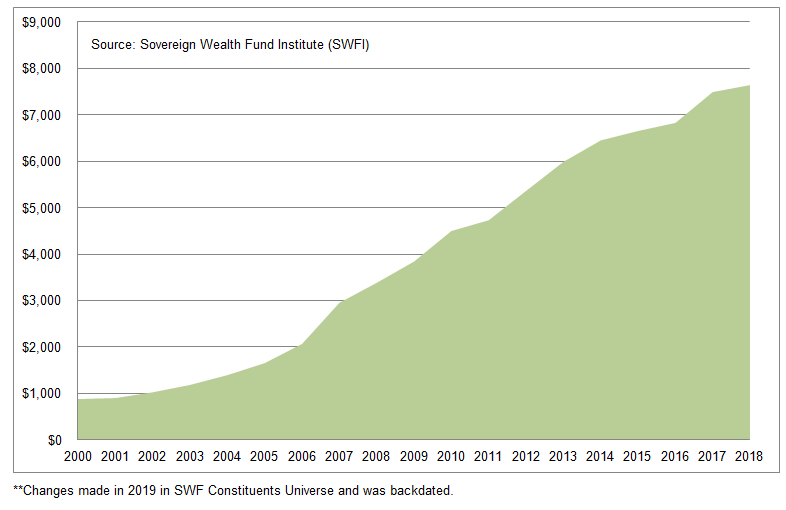

The first SWF was KIA formed in 1953. Since then, other large SWFs have emerged, including ADIA (1976), GIC (1981), the Brunei Investment Agency (1983) and GPFG (1990). As seen in the chart below, there was a remarkable acceleration in new SWFs and the total AUM of SWFs since 2005. By end 2018, there were around 80 SWFs with a combined AUM of around US$8 trillion, as compared to about 30 SWFs with an aggregate AUM of less than US$2 trillion before 2005.

The increase in new SWFs can be attributed to the large balance-of-payments surpluses of two groups of countries:

- Oil-exporting countries that saw a huge rise in their oil revenue when oil prices jumped from US$20 a barrel in 1990 to almost US$140 a barrel in 2008. Several SWFs were then created to manage the revenue windfall.

- East Asian economies had since the 1980s consistently achieved strong export-led growth, balance-of-payments surpluses and fiscal savings. Their drive to accumulate foreign reserves was, as noted by various commentators, impelled by their experiences of the 1997/98 Asian Financial Crisis (AFC) and the policy conclusion that they needed a large “war chest” of reserves to forestall a recurrence of the AFC experience. Several Asian countries then considered the SWF model as a viable approach to investing their surplus reserves.

What do sovereign wealth funds invest in, and where?

As SWFs have become major investors, what and where they invest in are watched avidly by investors and policymakers. Stocks and bonds are the two most common assets held. It is estimated that about 80% of SWFs invest in stocks and bonds. Some of the large SWFs are significant shareholders of companies like Microsoft, Apple, Alibaba, Uber, Nestle and Royal Dutch Shell. For example, Norway’s GPFG alone owns about 1.5% of all listed global stocks.

SWFs also invest in alternative assets such as real estate, infrastructure and private equity. Their shift to these assets has been impressive, rising from an estimated aggregate of US$288 billion as at end 2007 to US$1.6 trillion in alternative assets AUM as at end 2016. Such assets are suitably aligned to the long-term investment horizons of SWFs, which are better placed to handle illiquid assets. SWFs find real estate and infrastructure investments attractive as they offer low volatility and inflation-adjusted steady income streams. Thus, large SWFs are now prominent investors in mega infrastructure projects, real estate and even technology-based private companies, a number of which have become recognisable unicorns.

The geographical spread of SWFs’ investments has also evolved. SWFs invest mainly in the developed economies – the United States, Europe and Japan – as their financial markets are deep and well-developed. However, they have also increased their exposure to the emerging markets over time as these markets opened up, while their potential long-term returns are viewed to be higher than the developed markets.

Brewing concerns

However, there have also been concerns about the growing financial power of SWFs:

- Weak governance standards in SWFs. SWFs vary on how transparent they are about their management structure, decision-making process and investments. As many SWFs are not legally required to submit annual reports containing audited financial statements, SWFs are at risk of cronyism or even corruption.

- SWFs have the investment clout to move markets significantly. SWFs acting alone or in unison can trigger large financial market movements. Additionally, several SWFs selling stocks in a weak market could induce panic among other investors.

- As SWFs are state-owned, their investments might be used to advance political aims.

However, the concerns that SWF investing can be disruptive have been largely unfounded. In fact, SWF’s investments have generally stabilised – not destabilised – markets. For example, during the 2007/08 Global Financial Crisis, SWF investments in several major US and European banks and brokerage houses helped thwart the escalation of a brewing banking crisis. The reserves from some SWFs were also tapped to fund the sudden increase in fiscal spending needed to boost growth.

Concerns that SWF investing can be disruptive have been largely unfounded. In fact, SWF’s investments have generally stabilised markets.

SWFs are also a source of long-term capital to both developed and developing countries. Due to SWFs’ ability to invest in significant capital for the long term, they have become sought-after investors in large infrastructure projects like power generation and distribution, telecommunications, airports and ports, and water utilities.

SWFs have also sought to quell concerns about governance and transparency by endorsing a governance framework called the Santiago Principles.

The Santiago Principles

Legal Framework, Objectives, and Coordination with Macroeconomic Policies

The guidelines call for SWFs to have a sound legal framework and structure, and a well- defined mission and clarity on how they are distinguished from other state entities.

Institutional Framework and Governance Structure

This section advocates measures promoting a sound governance structure. This entails a clear division of roles for better accountability, the appointment of governing bodies (such as a Board of Directors) in a predetermined manner, the production of an annual report, and preparation of financial statements by independent auditors which is based on accepted accounting principles, and rules-based outsourcing.

Investment and Risk Management Framework

The guidelines recommend a clear investment policy as a prerequisite to disciplined investment plans and practices, and a reliable risk management framework to promote sound investment operations and accountability.

The future of sovereign wealth funds

The future for SWFs will depend on the interplay of a host of complex factors. These factors include:

- Developments in the commodity markets, particularly oil prices

- Political and economic developments, including demographic trends, in home countries.

- How open countries will be to SWF investments

- How the global financial system will evolve

- Investment opportunities available and the associated risks

Some observations can be made about the effects of the factors mentioned above. First, SWFs have proven to be viable business models for investing countries’ reserves and pursuing intergenerational equity. The initial distrust towards SWFs has diminished. In short, SWFs have come to be seen as legitimate, influential and prominent participants in global financial markets.

Second, some developments can moderate the growth of SWFs. For example, the emergence of shale oil and other alternative energy sources and the switch to green energy may dampen oil prices, crimping the inflow of funds into oil-based SWFs.

Domestic demographic trends will be important. Ageing populations and shrinking working population might lead to more government spending, less tax revenue and hence less surplus funds for the SWFs concerned.

Finally, SWFs will likely continue to shift their investments towards two areas. One is emerging markets, as these have higher potential growth than the developed economies. The other is private market assets. Investing in these assets align with their capacity to invest sizeable capital for long-term returns.

For more information on SWFs mentioned in the article, please refer to their corporate websites.