GIC’s Economics & Investment Strategy department (EIS) conducts bespoke economic and long-term thematic research, and guides GIC’s top-down portfolio design and management by constructing long-term portfolio policy, undertaking medium-term asset allocation, and innovating alternative investment models. Kevin Bong, GIC’s Director of EIS, shares more on why and how scenario planning is applied to the work that GIC does in managing Singapore’s reserves for the long term.

Why is scenario planning important?

Scenario planning has become increasingly important for investors in recent years. The highly uncertain and challenging investment environment features a wide range of possible outcomes and downside risks that could significantly affect the markets (Figure 1).

By applying scenario planning to our top-down and bottom-up allocation processes, GIC is able to design and implement a more resilient investment model, and better deploy capital in ways that continue to generate good returns above global inflation over the long term.

Figure 1. Investors face a highly uncertain environment

How is scenario planning incorporated into gic’s investment model and process?

At one level, we identify and analyse plausible outcomes, both upside and downside, that may affect the portfolio over our investment horizon of 20 years. For example, the best portfolio for an environment of very low growth and inflation – commonly known as “secular stagnation” – would differ from the best portfolio for an environment of high growth and low inflation which one may associate with great technological leaps. These environments are within the realm of possibility, and in some cases, may be highly plausible. It is thus crucial for us to assess the impact of these possible scenarios when constructing a robust and resilient Policy Portfolio (Box 1).

Box 1. Scenario-Based Portfolio Construction for GIC’s Policy Portfolio

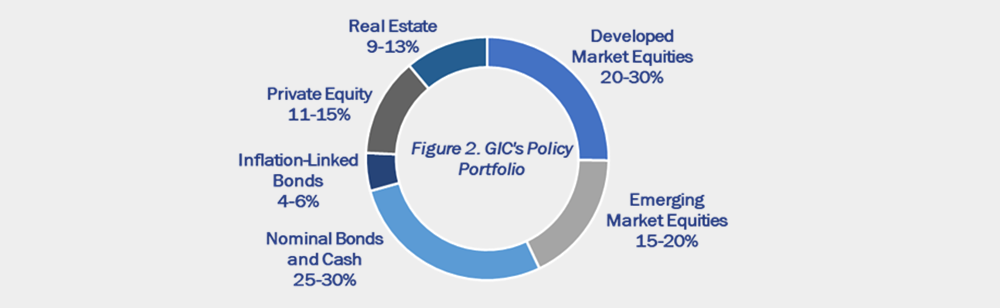

The Policy Portfolio represents GIC’s asset allocation strategy over the long term. It accounts for the bulk of the risk and return potential of the GIC Portfolio, and seeks to balance the way different asset classes respond to different economic environments. Diversification enables the Policy Portfolio to generate good risk-adjusted returns over a 20-year period (Figure 2).

Optimising the Policy Portfolio to a single scenario poses significant risk that the GIC Portfolio would be unable to meet our risk-return objectives if a different scenario were to play out. On the other hand, it is not possible to construct a single portfolio that outperforms all others in every scenario.

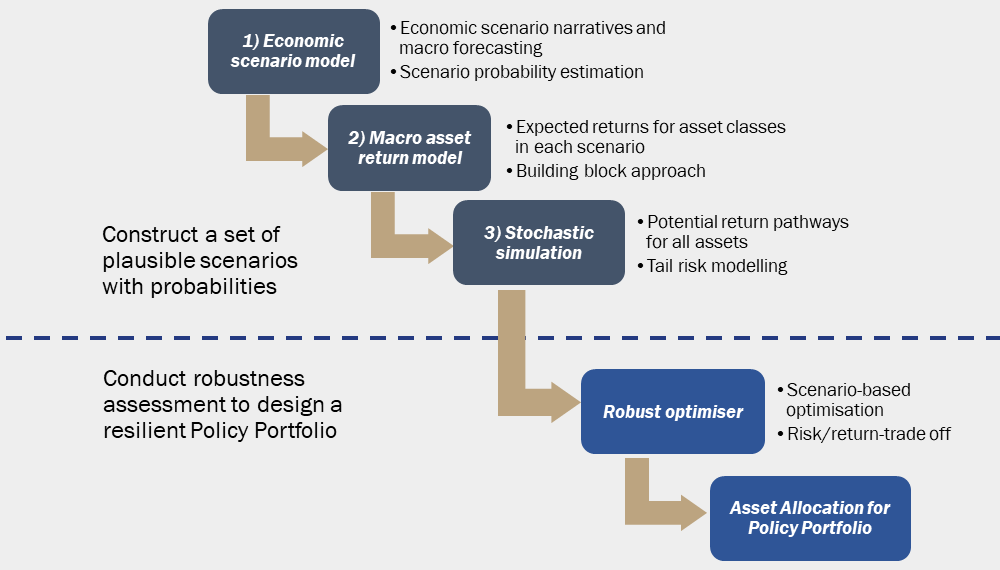

GIC’s scenario-based portfolio construction provides a systematic, consistent and coherent framework for the expression of investment decisions and assessment of risk-return trade-offs

(Figure 3). This approach consists of two key components. First, a three-step process to construct a set of plausible scenarios with probabilities. Second, a robustness assessment to ascertain a portfolio that would do well under a wide range of plausible scenarios.

Figure 3. GIC’s Scenario-Based Policy Portfolio Process

At another level, we explore a wider range of potential future environments that the rest of the world may not currently be paying attention to. This involves identifying nascent, high-impact drivers and possibilities of how the world may fundamentally change, before these are recognised and priced by the markets. For example, more than five years ago, technological disruption and the role of technology as an accelerator was less tangible for most investors than it is today. More recently, investor awareness and efforts surrounding climate change have gained momentum globally. We had been analysing these trends and developing our thinking for some years now. Thinking through such potential future scenarios enhances GIC’s thought process when reviewing our longer-term investment strategies.

These scenarios and impacts are also shared internally across the asset groups, and where relevant, are incorporated in the bottom-up underwriting process and stress-testing of investments.

Ultimately, scenario planning is a good demonstration of how GIC seeks to prepare, not predict, amidst a rapidly changing global investment environment.

What are the challenges of scenario planning?

The first key challenge is in designing scenarios. There are a myriad factors and thresholds to consider. For example, how many dimensions – growth, inflation and other factors – matter when defining distinct scenarios? What are the mechanisms by which the dimensions matter to the portfolio? How do we define the threshold of plausibility before a scenario is prioritised?

Determining the answers to these and other questions is as much an art as it is a science. We try to be systematic and comprehensive, but there is ultimately no “rulebook” to determining the best set of scenarios.

The second key challenge is in implementing the planning process and effecting change thereafter. Scenario planning requires us to consider outcomes that, though plausible, may be uncomfortable. When it comes to challenging our own assumptions, we all face intrinsic psychological and behavioural hurdles. After we overcome these hurdles, we may still face an uphill task in convincing others to consider and accept ideas that occasionally go against conventional wisdom. The challenge is further amplified by the need to define desired outcomes and paths to success, and then building the conviction and consensus needed to institute changes that enable us to achieve these outcomes.

What are some examples of tools utilised by your teams for scenario planning?

Scenarios are not just about destinations, they are also about paths leading to these destinations. In Portfolio Choice with Path-Dependent Scenarios, a collaboration with Windham Capital Management and State Street Associates, we outline a new systematic approach for investors to consider sequential outcomes, by defining scenarios not as average values, but as paths for the economic variables. Information on these paths is key to producing a quantitative, objective evaluation of return opportunities, downside risks and their probabilities. We apply this framework internally as part of our overall toolkit to assess long-term uncertainties and inform asset allocation decisions, so as to build a portfolio that is resilient across a wide range of potential scenarios.

As GIC has a significant allocation to alternative asset classes, it is also important that we assess the impact of scenarios on portfolio performance and liquidity. Last year, we collaborated with PGIM to enhance and expand PGIM’s OASIS™ (Optimal Asset Allocation with Illiquid Assets) Framework, which formally integrates liquidity measurement and cash flow management into a multi-asset, multi-period portfolio construction process. This framework allows us to simulate the returns and risk of public and private assets in a multi-asset portfolio, using our views on future private asset performance (relative to public assets), as well as fund-selection skills which can be an important performance driver. In addition, the framework introduces cash flow modelling consistent with the underlying market environment. This helps to guide better asset allocation decisions based on liquidity risk tolerance and return trade-offs.

What is needed for effective scenario planning?

Effective scenario planning is integral to creating a more resilient portfolio, and enables GIC to better meet our risk-return objectives over the long term.

I believe that successful scenario planners need to have three key qualities. First, be very open-minded when brainstorming these alternative scenarios. Second, be pragmatic about impact, plausibility, and therefore prioritisation and selection of scenarios. Finally, be tenacious in seeing through the implementation of necessary changes.