COVID’s Impact on sustainability

Amidst the turmoil created by the COVID-19 crisis, what stood out was the continued shift towards sustainable or ESG (Environmental, Social and Governance) investing. Global sustainable funds saw strong capital inflows of ~US$117 billion, versus a net outflow of ~US$30 billion for the broader fund universe over 1H 2020. Sustainable funds and indices also outperformed their counterparts in 1H 2020. For example, returns on the MSCI World Socially Responsible Investment (SRI) index outperformed the MSCI World index by 411bps over the same period, even controlling for sector tilts (e.g. underweight energy, overweight technology).

The pandemic has also highlighted some key ESG-oriented structural shifts. First, it has magnified the vulnerabilities and awareness of rising social inequality, specifically in the areas of access to technology, healthcare, jobs and social safety nets. Second, safety measures and supply chain disruptions have triggered a huge push to technology and automation, which could result in an even faster pace of job displacements, especially for lower-skilled workers. Third, the disruptions to cashflows, production and operating models have heightened the need for good governance, corporate resilience and robust capital allocation strategies.

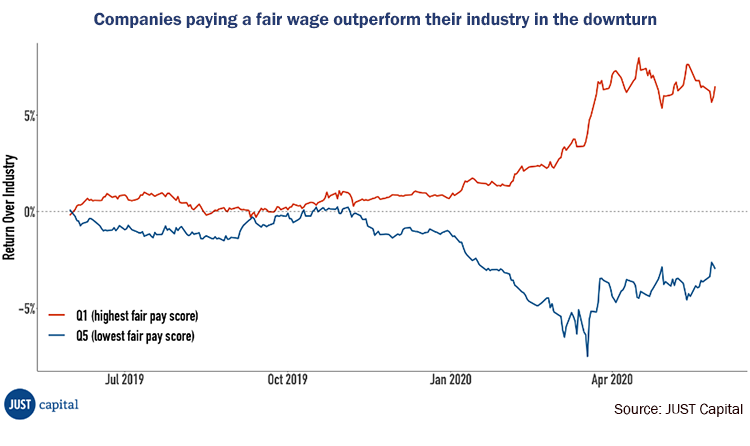

While the Environmental aspect, particularly climate change remains a key focal point, COVID-19 has resulted in Social factors having a greater influence on corporate behaviour, economics and financial performance. For example, as the figure below illustrates, companies that pay fair wages to their employees saw their share prices clearly outperform, as compared to that of companies that ranked poorly on fair pay – thus giving new impetus to “stakeholder capitalism” despite current pressures on companies’ profits and investor returns.

The structural rise of sustainable investing

The term ESG was coined in 2005 in a study entitled Who Cares Wins. This later led to other key initiatives such as Principles for Responsible Investment (PRI) in 2006. Various studies also followed, which established the financial relevance of sustainable investing, and illustrated its lower downside risks and volatility, even through the worst of past equity market downturns. Together with increasing support from international organizations, government bodies, and financial and investment institutions; improving reporting standards and data; and growing ESG-related investment vehicles, this has resulted in the sharp rise of sustainable investing, particularly over the last five years.

In 2018, the ESG investing market was worth over US$30 trillion in AUM, or ~33% of all professionally managed assets around the world – up from 21.5% in 2012. While there are varied estimates of ESG-related AUM, depending on how ESG is defined by asset class, strategy, market and investor coverage, the underlying growth trend is clear.

Investors seeking to integrate ESG into their investment strategies initially faced challenges in data availability and quality, and a paucity of guiding frameworks and disclosure standards for companies. As more players entered the market to provide solutions, the landscape shifted, also creating a different set of challenges for investors. For example:

- The proliferation of data and service providers with different classifications and standards, which makes it difficult to make consistent comparisons, and hence investment decisions.

- The need to deal with evolving and differing global regulations across the US, Europe and Asia on ESG investment instruments and rules.

- The prevalence of “greenwashing” or “social washing” – a major issue for consumers and investors. Measuring performance of ESG factors is challenging as there is no clear framework or criteria for evaluating positive impact on the environment, or human or labour rights.

While it will take time for the industry to converge on a few leading standards for ESG- and climate-related data disclosure, there are clear signs that sustainable investing will persist as a secular trend, driven by:

Regulation (applies to both investors and corporates)

- Increased disclosure requirements and standardisation

- Increased scrutiny and financial costs for non-sustainable business activities

Demand

- Growing evidence that ESG investing can be profitable with lower downside and volatility

- Demographics – increased investing power of millennials, alongside the great wealth transfer from the baby boomer generation

- Better transparency as data availability and disclosures rise

Supply

- Growing supply of ESG investing options

- Availability of ESG measurement and benchmark tools

- Technology improvements that support better data and analytics

Ultimately, more investors are seeking to include ESG factors in their investment choices rather than focusing purely on financial returns, with allocations to ESG-related mandates likely to continue rising over time<cite></cite>. Externalities, such as environmental impact or liabilities that could arise from structural gaps in business conduct and governance, are also increasingly being priced into company valuations. Issues with data are set to improve in line with education, industry<cite></cite> and regulatory developments currently under way. New technology based on machine learning and big data will also unlock valuable insights and ways to apply ESG data to conventional financial information.

Looking ahead, these shifts are likely to further support the continued structural rise of sustainable investing, as investors, businesses and consumers change behaviours to account for future liabilities arising from how they deploy capital today.

GIC’s approach to sustainability

As Singapore’s sovereign wealth fund, ensuring long-term sustainability in our global investments and operations is fundamental to how we fulfil our mandate, which is to preserve and enhance the international purchasing power of the reserves under our management.

We believe that companies with good sustainability practices offer prospects of better risk-adjusted returns over the long term, and that this relationship will strengthen over time. This is driven by physical factors like climate change, as well as financial market factors given evolving regulations and investor and consumer preferences. These factors shape the long-term prospects and hence, value of companies.

We also believe in taking a long-term and holistic approach to sustainability in our investment and corporate processes. We recognise that for any investment, there are trade-offs and conflicts between different sustainability goals; there may be inherent conflict between environmental sustainability goals and social sustainability goals in the short term, especially for some emerging market countries. Hence, we favour engagement over divestment, and achieve this by directly involving management on discussions on how to operate more sustainably. Such an approach, unlike divestment, will lead to more beneficial outcomes for stakeholders over the long term.

Our approach to sustainability is led by GIC’s Sustainability Committee, which shapes and implements our sustainability framework, supports and promotes sound investment stewardship, and drives GIC’s response to emerging ESG risks and opportunities.

Putting sustainability into practice at GIC

We apply an O-D-E framework to integrate sustainability across our investment and corporate processes. ‘O’ refers to going on the Offensive when it comes to investment opportunities; ‘D’ refers to Defensive risk management; ‘E’ is how we improve our operations and processes to achieve Enterprise Excellence.

GIC’s O-D-E Framework to Sustainability

Offense

As regulators, consumers, and businesses increasingly act on sustainability considerations, new investment opportunities will open up. We aim to capture these by:

- Integrating sustainability considerations, including climate-related factors, into our investment processes. Across all asset classes, we are expanding the range of data and tools available to our teams, to incorporate both quantitative and qualitative ESG factors into investment analysis, due diligence, valuation, risk assessment and post-investment monitoring.

- Investing in ESG-related opportunities arising across asset classes. This includes renewable energy assets, “green” buildings, and emerging technologies that support the low-carbon transition. Past investments include Greenko, Energy Development Corporation (EDC), Apeel Sciences and Chargepoint. GIC has played a key role in optimising Greenko’s capital structure, shaping its strategy and improving corporate governance and reporting standards. In the case of Chargepoint, we introduced the company to our private equity and real estate departments for potential fleet leasing and real estate opportunities.

- Incorporating sustainability signals into quantitative strategies, for example, by identifying and acquiring high-quality ESG data, and supplementing these data sets with proprietary analyses.

- Greening our portfolio of real assets by ensuring that all buildings we invest in are environmentally sustainable, or have the potential to be retrofitted to improve their environmental footprint. For example, extensive energy reduction and sustainability efforts were implemented in Gangnam Finance Center, GIC’s wholly-owned office building located in the hub of Seoul’s Gangnam Finance District. As a result of these efforts, the Center was certified LEED-EB Gold in 2011, and LEED-EB Platinum, the highest certification level achievable in LEED, in 2013.

Defense

Sustainability trends and climate change pose investment risks, including physical risks of being damaged by extreme weather events, and financial risks of assets being “stranded” as economies transition to a low-carbon economy. We protect our investments by:

- Regularly screening our existing portfolio for a variety of ESG issues. This includes stress testing our portfolio against potential climate-related disruptions and scenarios, implementing appropriate hedging strategies to mitigate anticipated risks.

- Conducting additional due diligence for companies exposed to greater sustainability risks, and adjusting our long-term valuation and risk models accordingly. For example, we consider how a company is positioned for the transition to a lower-carbon economy, whether it has adequate measures to identify and mitigate potential climate change-related risks, and whether such efforts are prioritised by its management.

- Actively engaging our portfolio companies to improve corporate governance, strengthen resilience against climate risks, and advocate for other positive environment and social outcomes. We regularly speak with senior management and boards of directors, and vote responsibly across all active and significant holdings.

- Researching climate change risks and stress-testing our portfolio against potential near-term climate-related disruptions and long-term climate scenarios. We apply the results of the stress tests to develop strategies that mitigate anticipated risks and make our portfolio more climate-resilient. For instance, by assessing the potential financial impact of future changes in carbon prices on our investments, we are able to better engage with investee companies to develop specific mitigation actions.

- Supporting efforts by the Taskforce on Climate-related Financial Disclosures (TCFD)to develop an internationally accepted framework on climate reporting, and also encourage companies to adopt TCFD’s recommendations on disclosures. We view the TCFD as providing a practical framework for companies to disclose their climate-related strategies, and for investors to incorporate climate change considerations into long-term investment decisions.

Enterprise excellence

The way in which we operate sustainably as an organization is as important as the way we invest. We do this by:

- Procuring and consuming sustainably. We communicate clear expectations for sustainable behaviour by our business partners and service providers, and do not enter into contracts with those who do not meet our standards. We also cut down on the use of non-recyclable materials, reduce energy usage through technology and staff behaviours, and improve the environmental footprint of our office spaces.

- Aiming to be carbon-neutral across our global operations from FY2020/2021.

- Fostering collaboration and inclusion. We believe that an inclusive culture – where our people share a common purpose, sense of belonging, diversity of skills and views, and respect and active contribution – makes for greater collective impact.

- Advocating an understanding of long-termism in the community, through our active participation in initiatives such as FCLTGlobal and the International Forum of Sovereign Wealth Funds (IFSWF), contributions to research on long-term investment issues, and financial literacy programmes in collaboration with schools and other organizations.

- Building confident communities. Our employees are empowered to engage with non-profits by contributing their time and expertise to their respective communities. We also collaborate with our business partners for community events, and contribute to humanitarian efforts globally.

- Ensuring sound governance. We require the highest standards of responsible and ethical conduct from our employees in all our business dealings.

Conclusion

Sustainability is one of the most significant trends in the financial markets given its material impact on a company’s risk profile, cost of capital and long-term performance. Investors face a real risk of underperforming if they do not effectively integrate ESG considerations into their investments.

Given our mandate, sustainability remains a key priority and an essential part of GIC’s investment strategy, risk management, corporate culture and process. By integrating sustainability factors into our management and investment processes, we build resilience and diversification in our portfolio to achieve better long-term returns. In addition, we strive to create positive outcomes for our portfolio and the communities we invest in, by helping companies move toward a more long-term stakeholder-centric model of corporate behavior. This will reinforce GIC’s role as a long-term investor and a responsible steward of our country’s reserves.